The author of the article is Alexey Malanov, expert at the anti-virus technology development department at Kaspersky Lab.

I have repeatedly heard the opinion that blockchain is very cool, it is a breakthrough, it is the future. I hasten to disappoint you if you suddenly believed in this.

Clarification: in this post we will talk about the implementation of blockchain technology that is used in the Bitcoin cryptocurrency. There are other applications and implementations of blockchain, some of which address some of the shortcomings of the “classic” blockchain, but they are generally built on the same principles.

About Bitcoin in general

I consider Bitcoin technology itself to be revolutionary. Unfortunately, Bitcoin is used too often for criminal purposes, and as an information security specialist, I do not like it at all. But if we talk about technology, then a breakthrough is obvious.

All the components of the Bitcoin protocol and the ideas embedded in it, in general, were known before 2009, but it was the authors of Bitcoin who managed to put everything together and make it work in 2009. For almost 9 years, only one critical vulnerability was found in the implementation: the attacker received 92 billion bitcoins in one account; the fix required rolling back the entire financial history for a day. Nevertheless, just one vulnerability in such a period is a worthy result, hats off.

The creators of Bitcoin had a challenge: to make it somehow work under the condition that there is no center and that no one trusts anyone. The authors completed the task, electronic money is functioning. But the decisions they made are monstrously ineffective.

Let me make a reservation right away that the purpose of this post is not to discredit the blockchain. This is a useful technology that has and will still find many wonderful applications. Despite its disadvantages, it also has unique advantages. However, in pursuit of sensationalism and revolution, many focus on the advantages of technology and often forget to soberly assess the real state of affairs, ignoring the disadvantages. Therefore, I think it is useful to look at the disadvantages for a change.

An example of a book in which the author has high hopes for blockchain. Further in the text there will be quotes from this book

Myth 1: Blockchain is a giant distributed computer

Quote #1: “Blockchain can become Occam’s razor, the most efficient, direct and natural means of coordinating all human and machine activity, consistent with the natural desire for balance.”

If you haven't delved into , but just heard reviews about this technology, you might have the impression that blockchain is some kind of distributed computer that performs, accordingly, distributed calculations. Like, nodes around the world are collecting bits and pieces of something more.

This idea is fundamentally wrong. In fact, all nodes serving the blockchain do exactly the same thing. Millions of computers:

- They check the same transactions using the same rules. They do identical work.

- They record the same thing on the blockchain (if they are lucky and given the opportunity to record it).

- They keep the entire history for all time, the same, one for everyone.

No parallelization, no synergy, no mutual assistance. Only duplication, and at once million-fold. We will talk about why this is needed below, but as you can see, there is no effectiveness. Quite the contrary.

Myth 2: Blockchain is forever. Everything that is written in it will remain forever

Quote #2: “With the proliferation of decentralized applications, organizations, corporations and societies, many new types of unpredictable and complex behavior reminiscent of artificial intelligence (AI) may emerge.”

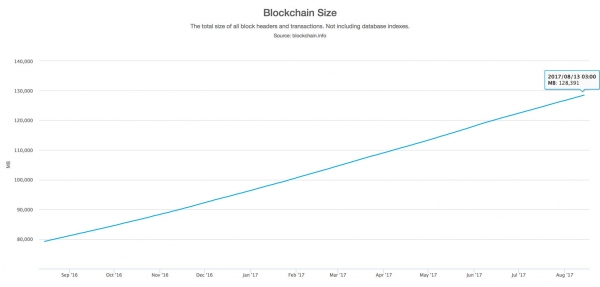

Yes, indeed, as we found out, every full-fledged client of the network stores the entire history of all transactions, and more than 100 gigabytes of data have already accumulated. This is the full disk capacity of a cheap laptop or the most modern smartphone. And the more transactions take place on the Bitcoin network, the faster the volume grows. Most of them have appeared in the last couple of years.

Blockchain volume growth.

And Bitcoin is lucky - its competitor, the Ethereum network, has already accumulated 200 gigabytes in the blockchain in just two years after its launch and six months of active use. So in current realities, the eternity of the blockchain is limited to ten years - the growth in hard drive capacity definitely does not keep pace with the growth in blockchain volume.

But besides the fact that it needs to be stored, it also needs to be downloaded. Everyone who tried to use a full-fledged local wallet for some cryptocurrency was amazed to find that he could not make and accept payments until he downloaded and verified the entire specified amount. You will be lucky if this process takes only a couple of days.

You may ask, is it possible not to store all this, since it is the same thing, on each network node? It is possible, but then, firstly, it will no longer be a peer-to-peer blockchain, but a traditional client-server architecture. And secondly, then clients will be forced to trust the servers. That is, the idea of “not trusting anyone,” for which, among other things, the blockchain was invented, disappears in this case.

For a long time, Bitcoin users have been divided into enthusiasts who “suffer” and download everything, and ordinary people who use online wallets, trust the server and who, in general, do not care how it works there.

Myth 3: Blockchain is efficient and scalable, regular money will die out

Quote #3: “The combination of blockchain technology + personal organism" will allow all human thoughts to be encoded and made available in a standardized compressed format. Data can be captured by scanning the cerebral cortex, EEG, brain-computer interfaces, cognitive nanorobots, etc. Thinking can be represented in the form of chains of blocks, recording in them almost all of a person’s subjective experience and, perhaps, even his consciousness. Once recorded on the blockchain, various components of memories can be administered and transferred - for example, to restore memory in the case of diseases accompanied by amnesia.”

If each network node does the same thing, then it is obvious that the throughput of the entire network is equal to the throughput of one network node. And do you know what exactly it is equal to? Bitcoin can process a maximum of 7 transactions per second - for everyone.

Additionally, on the Bitcoin blockchain, transactions are only recorded once every 10 minutes. And after the entry appears, to be safe, it is customary to wait another 50 minutes, because entries are regularly rolled back spontaneously. Now imagine that you need to buy chewing gum with bitcoins. Just stand in the store for an hour, think about it.

Within the framework of the whole world, this is already ridiculous, when hardly every thousandth person on Earth uses Bitcoin. And at such a speed of transactions, it will not be possible to significantly increase the number of active users. For comparison: Visa processes thousands of transactions per second, and if necessary, it can easily increase capacity, because classic banking technologies are scalable.

Even if regular money does die out, it will clearly not be because it will be replaced by blockchain solutions.

Myth 4: Miners ensure the security of the network

Quote #4: “Autonomous businesses in the cloud, powered by blockchain and powered by smart contracts, could enter into electronic contracts with relevant organizations, such as governments, to self-register under any jurisdiction they wish to operate under.”

You've probably heard about miners, about giant mining farms that are built next to power plants. What are they doing? They waste electricity for 10 minutes, “shaking” the blocks until they become “beautiful” and can be included in the blockchain (about what “beautiful” blocks are and why “shake” them, ). This is to ensure that rewriting your financial history takes the same amount of time as writing it (assuming you have the same total capacity).

The amount of electricity consumed is the same as the city consumes per 100 inhabitants. But add here also expensive equipment that is only suitable for mining. The principle of mining (the so-called proof-of-work) is identical to the concept of “burning humanity’s resources.”

Blockchain optimists like to say that miners are not just doing useless work, but are ensuring the stability and security of the Bitcoin network. It's true, the only problem is that miners protect Bitcoin from other miners.

If there were a thousand times fewer miners and a thousand times less electricity burned, then Bitcoin would function no worse - the same one block every 10 minutes, the same number of transactions, the same speed.

There is a risk with blockchain solutions "" The essence of the attack is that if someone controls more than half of all mining capacity, he can secretly write an alternative financial history in which he did not transfer his money to anyone. And then show everyone your version - and it will become reality. Thus, he gets the opportunity to spend his money several times. Traditional payment systems are not susceptible to such an attack.

It turns out that Bitcoin has become a hostage to its own ideology. “Excess” miners cannot stop mining, because then the likelihood that someone alone will control more than half of the remaining power will sharply increase. While mining is profitable, the network is stable, but if the situation changes (for example, because electricity becomes more expensive), the network may face massive “double spending.”

Myth 5: Blockchain is decentralized and therefore indestructible

Quote #5: “In order to become a full-fledged organization, a decentralized application must contain more complex functionality, such as a constitution.”

You may think that since the blockchain is stored on every node in the network, the intelligence services will not be able to close Bitcoin if they want, because it does not have some kind of central server or something like that - there is no one to come to to close it. But this is an illusion.

In reality, all “independent” miners are organized into pools (essentially cartels). They have to unite because it is better to have a stable, but small income, than a huge one, but once every 1000 years.

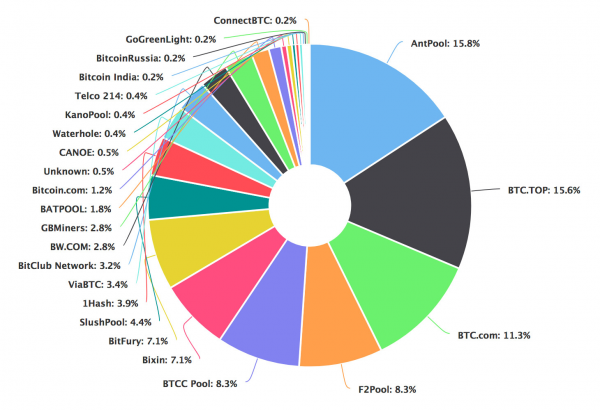

Bitcoin power distribution across pools.

As you can see in the diagram, there are about 20 large pools, and only 4 of them control more than 50% of the total power. All you have to do is knock on four doors and gain access to four control computers to give you the ability to spend the same bitcoin more than once on the Bitcoin network. And this possibility, as you understand, will somewhat depreciate Bitcoin. And this task is quite feasible.

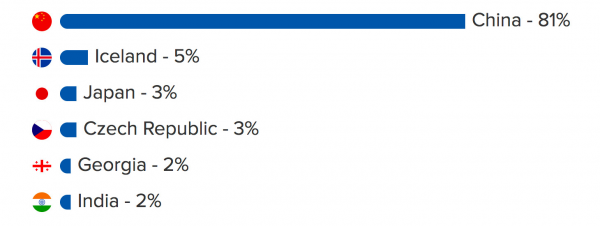

Distribution of mining by country.

But the threat is even more real. Most of the pools, along with their computing power, are located in the same country, making it easier to potentially seize control of Bitcoin.

Myth 6: Anonymity and openness of the blockchain are good

Quote #6: “In the era of blockchain, traditional government 1.0 is largely becoming an outdated model, and there are opportunities to move from inherited structures to more personalized forms of government.”

The blockchain is open, everyone can see everything. So Bitcoin doesn't have anonymity, it has "pseudonymity". For example, if an attacker demands a ransom on a wallet, then everyone understands that the wallet belongs to the bad guy. And since anyone can monitor transactions from this wallet, a fraudster will not be able to use the received bitcoins so easily, because as soon as he reveals his identity somewhere, he will immediately be imprisoned. On almost all exchanges, you must be identified to exchange for regular money.

Therefore, attackers use the so-called “mixer”. The mixer mixes dirty money with a large amount of clean money, and thereby “launders” it. The attacker pays a large commission for this and takes a big risk, because the mixer is either anonymous (and can run away with the money) or is already under the control of someone influential (and can turn it over to the authorities).

But leaving the problems of criminals aside, why is pseudonymity bad for honest users? Here's a simple example: I transfer some bitcoins to my mom. After this she knows:

- How much money do I have in total at any given time?

- How much and, most importantly, what exactly did I spend it on all the time? What did I buy, what kind of roulette did I play, what politician did I support “anonymously”.

Or if I repaid a debt to a friend for lemonade, then he now knows everything about my finances. Do you think this is nonsense? Is it difficult for everyone to open the financial history of their credit card? Moreover, not only the past, but also the entire future.

If for individuals this is still all right (well, you never know, someone wants to be “transparent”), then for companies it is fatal: all their counterparties, purchases, sales, clients, volume of accounts and in general everything, everything, everything - becomes public. Openness of finance is perhaps one of the biggest disadvantages of Bitcoin.

Conclusion

Quote No. 7: “It is possible that blockchain technology will become the upper economic layer of the organically connected world of various computing devices, including wearable computing devices and Internet of Things sensors.”

I have listed six major complaints about Bitcoin and the version of the blockchain it uses. You may ask, why did you learn about this from me, and not earlier from someone else? Doesn't anyone see the problems?

Some are blinded, some just don't understand , and someone sees and realizes everything, but it is simply not profitable for him to write about it. Think for yourself, many of those who bought bitcoins begin to advertise and promote them. Kinda comes out. Why write that technology has disadvantages if you expect the rate to rise?

Yes, Bitcoin has competitors who have tried to solve certain problems. And while some of the ideas are very good, blockchain is still at the core. Yes, there are other, non-monetary applications of blockchain technology, but the key disadvantages of blockchain remain there.

Now, if someone tells you that the invention of blockchain is comparable in importance to the invention of the Internet, take it with a fair amount of skepticism.

Source: habr.com